Providing Certain Non Assurance Services To An Audit Client

Provision of Non-assurance Services to Audit Clients. 290162 To avoid the risk of assuming a management responsibility when providing non-assurance services to an audit client the firm shall be satisfied that client management makes all judgment s and decisions that are the responsibility of management.

Chapter 5 Audit Related Services Ppt Video Online Download

A list of the prohibitions that apply when providing certain types of NAS to audit clients that are PIEs is included in Appendix 1 of this document.

Providing certain non assurance services to an audit client. Non audit service prohibition would result in an increase in of professional costs in key areas. In addition a self-interest threat may arise due to the income generated from providing the non-assurance. The exact wording of Article 5 which lists the prohibitions is included below.

See Part 4 Section 600 paragraph R6007 and related provisions in paragraphs 6007 A1 to R6008. Identification of public subsidies and tax incentives unless support. As regards the non-audit services such services can usually be provided at far less cost by auditors who have the benefit of their cumulative audit knowledge.

The IFAC SMP Committee is seeking feedback on their preliminary views in response to the IESBAs Exposure Draft on proposed changes to the Code of Ethics for Professional Accountants addressing non-assurance services for audit clients. As regards the audit service the need for one firm to advise on and another to audit key issues would inevitably increase costs. Tax services relating to.

For a business owner or non-profit institution this means potentially saving on costs by also contracting their auditor for additional jobs assuming they have the expertise and are a good fit for the requirements of the services. ES 5 - non-audit services provided to audited entities. Providing additional guidance and clarification regarding what constitutes management responsibility including enhanced guidance regarding how the auditor can better satisfy itself that client management will make all judgments and decisions that are the responsibility of management when the auditor provides non-assurance services to an audit client.

Preparation of tax forms. In some cases even if. Subject to general principles of independence an auditor will be able to provide any non-audit service that is not explicitly prohibited.

The audit committee should consider whether company policies and procedures require that all audit and non-audit services are brought before the committee for pre-approval. Findings from Survey of Audit Committee Members. The threats created are most often self-review self-interest and.

The changes in the pronouncement enhance the independence provisions in the Code of Ethics for Professional Accountants the Code by in particular no longer permitting auditors to provide certain prohibited non-assurance services to public interest entity PIE audit clients in emergency situations and ensuring that they do not assume management responsibility when. The EU audit legislation prohibits many non-audit services from being provided to companies by their statutory auditors. 290156 Firms have traditionally provided to their audit clients a range of non-assurance services that are consistent with their skills and expertise.

I consider whether a reasonable third party would regard the objectives of the proposed engagement as being inconsistent with the objectives of the audit. The audit firm providing non-audit services to audit clients may create a self-review threat because the service provided may affect transactions recorded in the financial statements on which the auditor must then express an opinion. Exposure Draft October 2011.

The International Ethics Standards Board for Accountants has released for public comment an exposure draft on proposed changes to certain provisions of the ethics code related to non-assurance services for audit clients. AMENDMENTS TO PROFESSIONAL AND ETHICAL STANDARD 1 REVISED ADDRESSING CERTAIN NON-ASSURANCE SERVICES PROVISIONS FOR AUDIT AND ASSURANCE CLIENTS This Standard was issued on 25 June 2015 by the New Zealand Auditing and Assurance Standards Board of the External Reporting Board pursuant to section 12b of the Financial Reporting Act 2013. The firm or a network firm may provide an audit client that is not a.

Providing non-assurance services may however create threats to the independence of the firm or members of the audit team. Firms might provide a range of non-assurance services to their assurance clients consistent with their skills and expertiseProviding certain non-assurance services to assurance clients might create threats to compliance with the fundamental principles and threats to independenceThis section sets out specific requirements and application material relevant to applying the conceptual. Also listing company standards require audit committees to pre-approve all audit review and attest services regardless of whether the firm performing the services is the companys principal auditor.

This fact sheet details which services are prohibited under the EU baseline rules and those that could potentially be allowed under certain circumstances including. Before the audit firm accepts a proposed engagement to provide non-audit services to an audit client the audit engagement partner shall. CHANGES TO THE CODE ADDRESSING CERTAIN NON-ASSURANCE SERVICES PROVISIONS FOR AUDIT AND ASSURANCE CLIENTS 4 SECTION 290 CLEAN Provision of Non-assurance Services to an Audit Client Management Responsibilities Paragraphs 290159 290163 will be deleted and replaced with the following paragraphs 290159 290162.

Restrictions on Non-Audit Services. February 29 2012 Basis for Conclusions Prepared by the Staff of the IESBA. Matters concerning auditor independence when providing NAS to audit clients.

Internal procedures that ensure objective choices in commissioning non-assurance engagements. Performing services for an assurance client that directly affect the subject matter of the. Feedback indicating diversities in interpretations and practices in applying certain Non-Assurance Services.

In summary section 902 prohibits an auditor from being appointed where certain specified services were rendered to the same client. Provision of Non-assurance Services to an Audit Client. Certain non-audit services would be seen to be such a significant threat to the independence of the auditor that the only possible solution is to prohibit the provision of such services to audit clients if they have an impact on the financialstatements to be audited.

In recent years however auditors have been aiming to diversify into new lines of business to provide non audit services to clients. Addressing Certain Non-Assurance Services Provisions for Audit and Assurance Clients. Providing Non-Assurance Services.

Senior Counsel opinion obtained jointly by the IRBA and SAICA states that the provisions of section 902 b regarding the prohibition from being validly appointed as auditor in respect of audit and certain non.

Healthcare Accounting Services Harshwal Company Llp Accounting Services Health Care Accounting

Pin On Seo

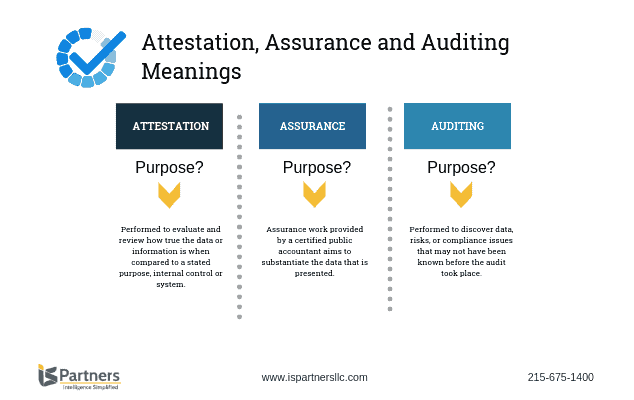

Defining Attestation Auditing Assurance I S Partners Llc

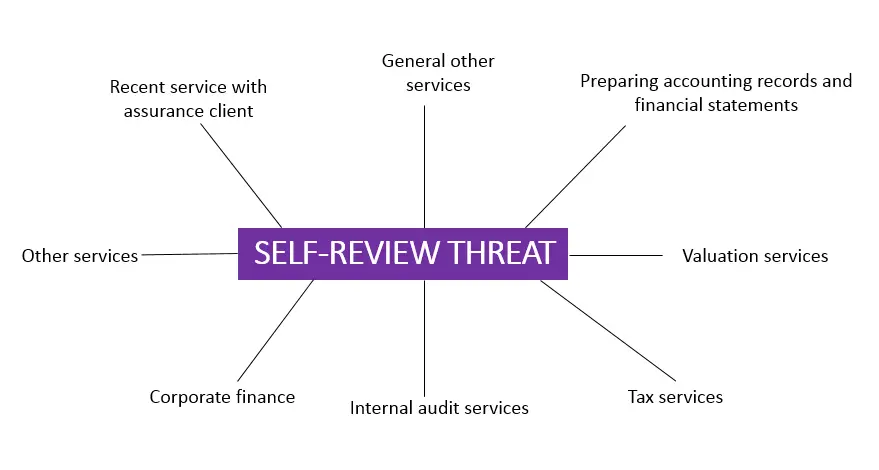

Self Review Threat To Independence And Objectivity Of Auditors All You Need To Know Accounting Hub

Valuation Of Esop In Gurgaon Especia Associates Llp Business Valuation Audit Services Secretarial Services

Our Business Model And Approaches Are Tailored To Focus On Actions That Are Ideally Suited To A Business Accounting Services Accounting Consultant Accounting

Difference Between Audit And Non Audit Services With Table Ask Any Difference

Account Services Usa Accounting And Auditing Firms Hcllp Audit Services Financial Statement Financial

Pin On Resume Template

Professional Internal Audit Report Template Example With Blank Details Table Form In Multi Colors Accent Internal Audit Report Template Sales Report Template

Our Multi Award Winning Team Of Directors And Consultants Combine Expertise Common Sense And A Flexib Accounting Consultant Professional Accounting Accounting

Pdf Non Audit Service And Auditor Independence An Examination Of The Procomp Effect

What Are The Standard Auditing Process Audit Services Internal Audit Audit

Internal Control Audit Report Template 1 Templates Example Templates Example In 2021 Internal Control Report Template Audit

What Non Audit Services Can An Auditor Provide Sd Mayer

Deloitte Kantoor Rotterdam Dining Table Rotterdam Home Decor

Harshwal Company Llp S Accounting Services Provide The Support Objectivity And Expertise Businesses Requiremen Accounting Services Audit Services Accounting

Auditing Assurance Services Best Bookkeeping Firm Hcllp Audit Services Evaluation Employee Professional Accounting

Section 600 Provision Of Non Assurance Services To An Audit Client Iesba Code Of Ethics For Professional Accountants

Posting Komentar untuk "Providing Certain Non Assurance Services To An Audit Client"